One Year On: The Crowdsourced Portfolio

Assessing the performance of the crowdsourced portfolio from last year

In late August 2024, I penned a letter about the kind of Twitter threads you see during moments of exuberance.

Now and then, a Twitter thread will be dusted off from the warehouse of some exuberant period in financial markets. The thread usually contains a bunch of stocks that have performed terribly since that date. People point, laugh, say “What a sign of the times” and move on. One of the most visceral examples is the time Brian Feroldi asked Twitter, at the peak of 2021 mania; “What company is worth less than $10 billion today but you think could be worth $500+ billion in a few decades?”. He aggregated the top 20 responses and it is fair to say those picks were dreadful.

- Me, August 26th 2024

Since that infamous thread of future “$500+ billion” companies was posted, the basket has lost 61% in value while the S&P 500 has compounded at 12.5% per year, grossing 67% in returns.

Anyway… this letter culminated in an attempt to create a crowdsourced basket of ideas that “doesn’t suck”. To my surprise, we achieved it. So I think it’s about time we rebalanced this portfolio with new submissions.

The ideas were crowdsourced from readers of this newsletter. The T&C’s1 were defined, a start date2 was set, and I gave you each a week to submit your suggestions.

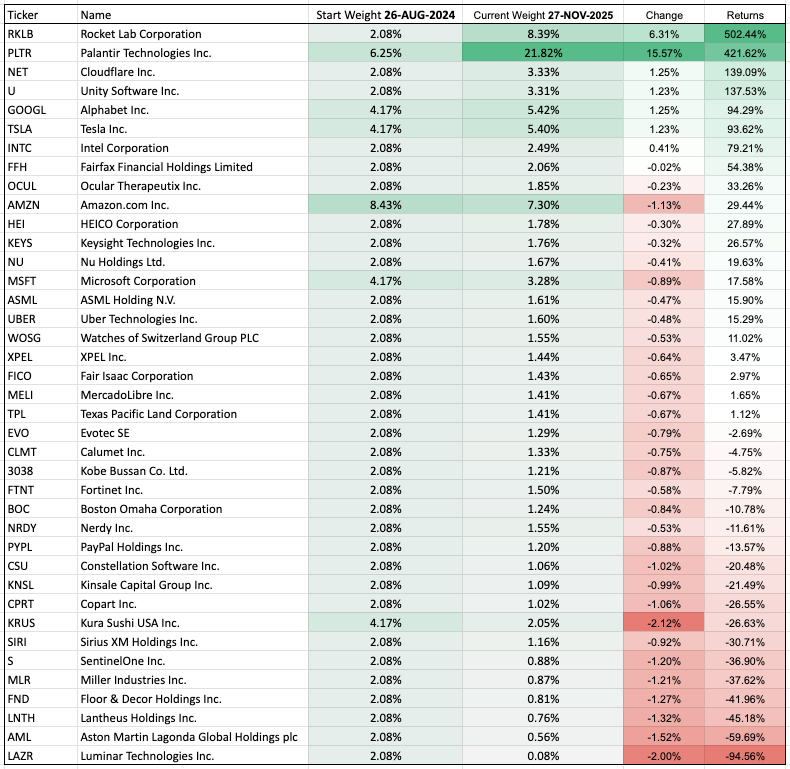

In total, 39 unique companies were submitted. Companies with more than 1 vote would command a proportionately higher weighting in the starting allocations. This was the case with popular suggestions like Amazon (8.43% starting weight) and Palantir (6.25% starting weight). Below, I have created a table of each holding, the absolute fluctuation in weight from inception to the 27th November 2025, and the individual returns of each stock over the period.

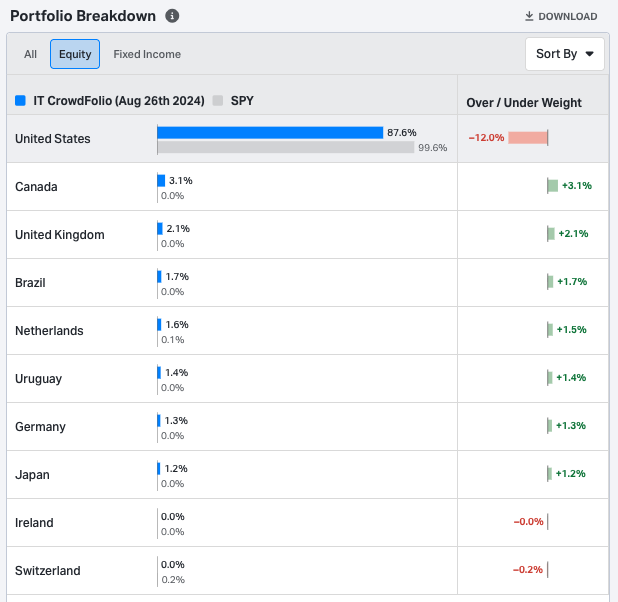

There was no official benchmark for this portfolio, but given that investing in an S&P 500 ETF would be the laziest way to manage one’s money, I will hereby knight the benchmark of this experiment as so. There is a matter of some minor differences in geographic exposure3, but we’ll let that slide. Compared to the benchmark’s 24.06% return over the lifetime of the Crowdsourced portfolio, just 12 (~31%) of the individual holdings outperformed. One pick in particular, Luminar Technologies, saw its share price plummet by 94.46%.

However, the stellar returns of Rocket Lab (+502.44%), Palantir (+421.62%), Cloudflare (+139.09%), Unity Software (+137.53%), Alphabet (+94.29%), and Tesla (+93.26%) resulted in a 25.37% surplus to the S&P 500 over the period, with the Crowdsourced portfolio generating returns of 49.43%.

For more details, I prepared a high-level report on the portfolio below. Feel free to read that.

I want to put the investing acumen of Investment Talk readers to the test… again. I want you to try your hardest and avoid submitting ideas that are based solely on upside with little consideration for downside risk. Imagine someone asked you to put your entire net worth into a single stock for five years. You’d be more likely to base this opinion on stocks that will perform well but also have a low chance of taking you out of the game entirely.

To Participate:

Comment below ONE equity you think has the greatest chance of beating the market, or performing amicably, over the next year or so.

Please include TICKER and NAME to avoid confusion.

T&C’s

I am going to leave this open for the next week or two. Once closed, I will aggregate the names and then create a rebalance for the existing model portfolio to track the performance over time.

The portfolio will be limited to a maximum of 40 individual names.

Funds or non-equity submissions will not be counted.

Each mention of a ticker will count as 1 vote. Duplicate entries will earn more votes, thus increasing the likelihood they are selected for the top 40.

If more than 40 names are suggested, the top 40 will be selected based on weight. If there are submissions with equal weights on the threshold, excluded submissions are at the discretion of the admin.

The portfolio will maintain the inception date of August 26th, 2024.

The portfolio will be rebalanced as per the votes on December 8th 2025, with no rebalancing or allocation changes thereafter.

One entry per person, the first entry will be counted.

The portfolio will use USD as the base currency.

Thanks for reading

Conor

The portfolio will be limited to 25 individual names.

Funds or non-equity submissions will not be counted.

Each mention of a ticker will count as 1 vote. Duplicate entries will earn more votes, thus increasing the likelihood they are selected for the top 25.

The portfolio will have an inception date of August 26th, 2024.

The portfolio will be equally weighted at the inception date, with no rebalancing or allocation changes thereafter.

One entry per person, the first entry will be counted.

The portfolio will use USD as the base currency.

26th August 2024

Crowdsource vs. S&P geographic exposure, country

Last year my submission was Kura Sushi (KRUS). It's a volatile stock, at times being +60% during the period. Execution has continued to be good, despite some softness throughout 2025. Over time, it has been growing into it's valuation.

Today it trades 26% lower than when I initially voted for it, and the forward sales multiple has compressed by 35% while revenue has grown 25% in a harsher environment. Some flashes of profitability, stronger operating cash flows...

This is all to say I am going to be boring and make the same submission the second time around.

MELI