Under the Hammer

(LON:ATG) Auction Technology Group

In my quest to turn over rocks, I recently spent some time looking at a small cap listed in the UK which has a global presence and the resemblance of a compelling network effect. They are a market leader, working to consolidate and vitalise an industry with a history that stretches back thousands of years. Ultimately, I passed on it, for reasons explained in this article. Nevertheless, it’s an interesting business that I added to my watchlist and may appeal to some of you. Here are my notes.

Auction Technology Group

The United Kingdom is home to several moaty businesses which dominate their respective markets. Companies like Rightmove (real estate portal) and Autotrader (digital vehicle marketplace) have long commanded significant market shares in their domain. In isolation, a high absolute market share is not a moat; what makes these particular companies special is the presence of strong network effects. A network effect is when a company provides a product or service that increases in value as the number of users expands and commonly has two or more ‘sides’ to the network. As the size of the network grows, so does the value to its members, and so does the toll the facilitator collects.

From print to public

A lesser-known two-sided network is Auction Technology Group (ATG), currently sporting a market cap of ~£550 million. Starting life as a weekly trade publication (Antiques Trade Gazette) in 1971 the birth of the internet would lead the company to gradually transition into facilitating online auctions. In 1998 they began listing auction calendars online. By 2006 they launched their first live bidding site. Through a series of acquisitions and partnerships, ATG went on to launch several more marketplaces (they host 8 digital marketplaces today) and merged with Proxibid in 2020. Having been in the market for a long time, many of ATG’s marketplaces command a sizeable market share.

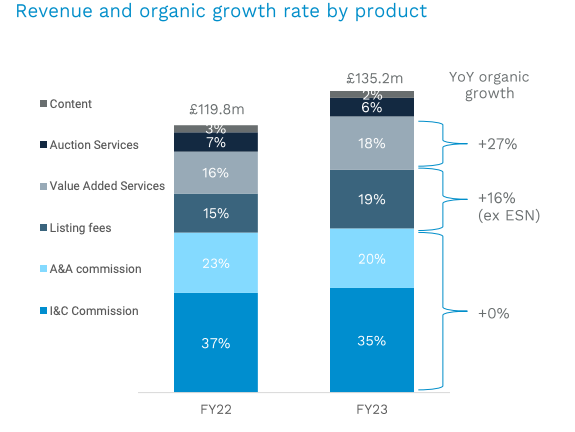

In 2021, they floated on the London Stock Exchange and became a public company. Revenues ballooned during the pandemic; quadrupling from £24.8 million in 2019 to £135.2 million in 2023. While things have decelerated over the past 12 months, ATG managed to increase sales by 12.8% in 2023. It’s important to note that ATG is not an auctioneer; they are the platform which connects auction houses and bidders.

The margin structure is illustrative of their nascent network effect. Gross margins are shy of 68% and operating margins are in the mid to high teens. Last year, the company turned a net profit for the first time since becoming a public company. There remains potential for expansion across all margins. It’s worth noting that as of FY24 onwards, ATG will change their revenue reporting currency from GBP to USD. This decision was made because the majority of the company’s revenue, costs, and cash flows are now generated in US Dollars.

Network effects

ATG’s technology facilitates online auctions for bidders across 165 countries for more than 3,900 auction houses and 4,800 estate sellers. The number of auction houses and bidders has been growing steadily. They provide services across the full spectrum of the auction process. In the lead-up to an auction, ATG can handle back office, support, and digital marketing. They then host the auction, handle bid management and registrations, as well as offering white-label auction solutions and cross-listing. Post-auction, ATG offer delivery, payments, analytics and account management, as well as other value-added services.

Last year (FY23) ATG listed 22 million lots (7.2 million sold) and processed £10.8 billion in Total Hammer Value; the total final sale value of items listed on their marketplaces. In addition to online, ATG offers live and hybrid auctions but seeks to capitalise on the structural migration to online. This process of connecting buyers and sellers has all the hallmarks of a classic network effect.

Because each of ATG’s marketplaces1 (see footnote) has a leading (or commanding) position in their respective markets it enables buyers to tap into auctions with the widest variety of offerings and allows sellers to present their goods in environments where they can be assured of attracting the largest number of potential bidders. ATG is largely focused on the auction of art, collectables, industrial equipment, and antiques. Just last year, high-ticket items sold at auction included; a first edition copy of the Philosopher’s Stone (£10.5k), a laser cutting machine ($770k), an original oil painting from J Leyendecker ($130k), and the metal endoskeleton arm from the second Terminator film (£55k). It’s an eclectic mix. The company discloses four operating segments; arts and antiques (A&A), industrial and commercial (I&C), auction services, and content. More than 90% of revenues are generated via the A&A and I&C segments.

Cyclical or not cyclical

According to CEO, John-Paul Savant, “death, divorce, downsizing and debt - provides the vast majority of the assets that get sold through our Arts and Antiques marketplaces”. The A&A inventory comprises second-hand art, collectables, furniture, jewellery, watches, and other luxury goods. A prevailing question mark on this business is whether or not it is pro-cyclical; it does well when the economy does well, and it does poorly when the economy is in bad shape. On the contrary, some argue the business is cycle-neutral; unaffected by the ups and downs of the economy.

There is evidence throughout the business that plays into both narratives. The A&A segment tends to be more sensitive to macroeconomic changes as the sector is discretionary. While weakened demand is certainly a factor during an economic glut, the supply side (people looking to raise money in a pinch) no doubt benefits, offsetting the former. Because A&A’s average lot size is on the lower end of the spectrum it can be said that they are less sensitive than marketplaces exposed primarily to higher-ticket art and antiques. The I&C business tends to be less cyclical with inventory comprised of used equipment, machinery, and commercial vehicles from industries such as manufacturing, metalworking, warehousing, construction, real estate, and agriculture. While pricing pressure may occur during recessions, the supply side is bolstered by bankruptcies, liquidations, and companies looking to raise cash. The dynamic between demand and supply compensates one another throughout the cycle.

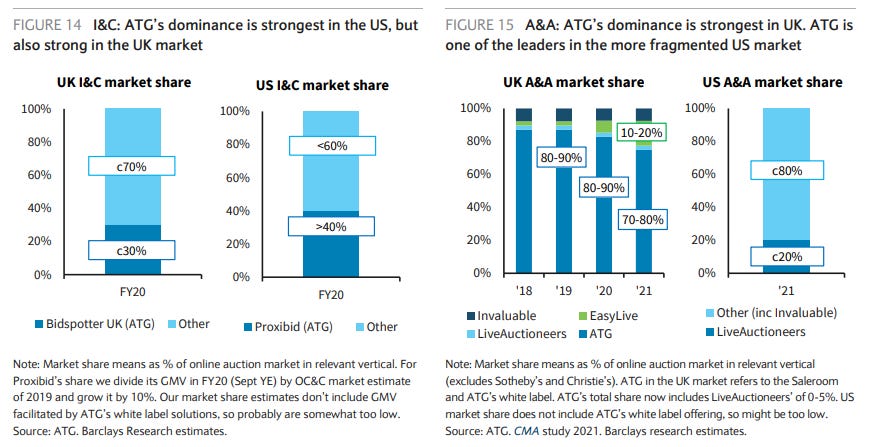

These charts2 are slightly dated, but circa 2020 Barclays estimates the market share of I&C to be ~30% (via Bidspotter) in the UK and ~40% (via Proxibid) in the US. The market share of A&A in the UK (~70% to 80%) is considerably higher thanks to The Saleroom dominating Europe and ~20% in the US following the acquisition of LiveAuctioneers.

Breather or signs of trouble

2023 represented somewhat of a breather year for ATG, after an incredible run following the pandemic. At constant FX rates, headline sales (+5%) and total hammer value (+3%) saw modest growth while gross merchandise value (-3%) declined. But the story was mostly about the second half, which illustrated “softness in our end auction markets”, cites CFO Thomas Hargreaves. Total hammer value witnessed a 5% decline vs the previous 6-month period a year prior. This same progression was evident throughout ATG’s operating segments; leaving investors concerned over weakening demand. Like most middlemen, ATG generates their revenue through a mixture of variable and fixed fees, commissions, and value-added services. This includes, but is not limited to, auction fees and commissions, auction-related services, digital advertising, software sales, subscription fees, digital advertising, payments services, and various other value-added services.

A&A is the largest segment, representing ~49% of ATG’s sales. The £65.6 million in revenue reported in FY23 saw a +19% growth rate on the previous year (+6% organic). A mixture of pricing increases and slowing demand did take their toll on the A&A division, however. While revenues grew over the period, gross merchandise value (GMV) declined 3% YoY. Total hammer value in A&A decelerated from 1% growth in the first half of 2023 to a 2% decline in the second; something which Hargreaves suggests “reflects the wider softer macroeconomic position and - the impact that's having on end consumer bidder demand”. A similar story is evident in the company’s second-largest division. I&C, which generates ~43% of ATG’s revenues, saw reported revenue growth of 10% in 2023 (+7% organic) with a 3% decline in GMV. Following a 16% growth rate in total hammer value in the first half of the year, the 7% decline in the second half further indicated economic softening.

The company’s other two operating segments saw modest declines too. Auction services (6% of sales), saw revenues decline 3% to £8.3 million on the back of a shift from digital to physical auctions as the societal impact of the pandemic continues to filter through the auction economy. Content, a mere 2% of sales, saw sales decline 3% to £3.1 million.

The market’s reaction to ATG’s earnings was cold; shares have since fallen ~25%. The weak second half and management’s commentary on the outlook remaining “relatively uncertain” had a large part to play there. ATG is guiding for organic revenue growth between 5% to 8% in FY24 (£142 million to £146 million); meaning they expect to grow at least as fast as FY23. It’s said that the adoption of value-added services (shipping, payments, etc) is helping to offset macro variables.

The prevailing narrative has been that ATG is non-cyclical, on account of their geographic dispersion, diverse customer base, and breadth in operating segments. However, this earnings report suggests that might not be the case. With the vast majority of their revenue derived from auction fees and clear signs of softness in the second half, ATG might be somewhat cyclical after all.

Silver lining

It is important to note that ATG’s pace of growth has been outstanding and that these growth rates were not sustainable. Since 2020, marketplace revenues (those derived from the A&A and I&C segments) have grown 158% from £48 million to £123.8 million. Revenues from auction services have grown 453% from £1.5 million to £8.3 million over the same period, while content revenue is approximately flat. Meanwhile, gross and EBIT margins have expanded, and the company reported its first net profitable year. Other KPIs such as Gross merchandise value, total hammer value, and take rates have all improved significantly too. The question is whether you believe this is simply a breather as the economic demand for this sector cools down, or the beginning of a structural decline. I believe that while there may be some cyclicality in the demand for ATG’s market, the market itself is not going anywhere. Hargreaves reaffirmed this point of view in the latest annual earnings call:

“It's important not to overstate what we're seeing at the moment. We've seen a few percentage points decline in THV for one-half after having had an extraordinary period of growth. Even if you look at 2-year CAGRs, they're both significantly up. There hasn't been any historic precedent for significant downturns in the markets we operate in. And they are very old, established businesses”.

For reasons covered earlier, the core segments at ATG (A&A and I&C) appear to have a level of embedded resistance to macroeconomic volatility.

M&A and goodwill

ATG pursue accretive M&A and states plainly they wish to grow through both organic and inorganic means; acquisitions strengthen their network. Just last year, the company acquired EstateSales.net for a consideration of $40 million. In 2021, ATG raised a $204 million loan facility to help finance the acquisition of LiveAuctioneers LLC for ~$500 million. This deal allowed ATG to penetrate the North American arts & antiques market.