Currency Schmurency

27-JAN-2026

I assume most independent investors seldom think about the ebbs and flows of the foreign exchange market when conducting their financial affairs. For the average individual, the most common interaction with foreign exchange (FX) rates comes from travel, when they want to see how much ‘bang’ they can get for their ‘buck’, pound, euro, yen, or whatever. It’s the kind of thing that’s quickly forgotten upon returning home to the sanctity of domestic currency.

The same is true for most US investors, who largely invest in domestically traded securities despite unbridled access to foreign markets. Direct ownership of non-USD-denominated securities is more of a rarity with the abundance of American Depositary Receipts (ADRs) available and a plethora of attractive opportunities at home. For some countries, investing domestically is more of a necessity; a byproduct of the friction in buying foreign stocks. India, for example, has liberalised access to foreign equities for individual investors in recent years, but there remains a hard cap on the value any one person can invest in a given year. In Vietnam, access to overseas brokerages is tightly controlled and subject to approval processes. However, situations like these tend to be the outliers. The United States, the UK, European Union members, Singapore, Hong Kong, Australia, Japan, Canada… all boast easy and cheap access to the corners of the world’s most important and liquid equity markets.

On the whole, FX can feel like optional exposure. Yet, avoidance of foreign exchange is possible in principle, but not in reality. Domestic equity can, at times, just be foreign revenue with a local ticker. For most large public companies, the customer base is global. They have divisions on multiple continents, earning sales in various currencies, all translated back to a single reporting currency.

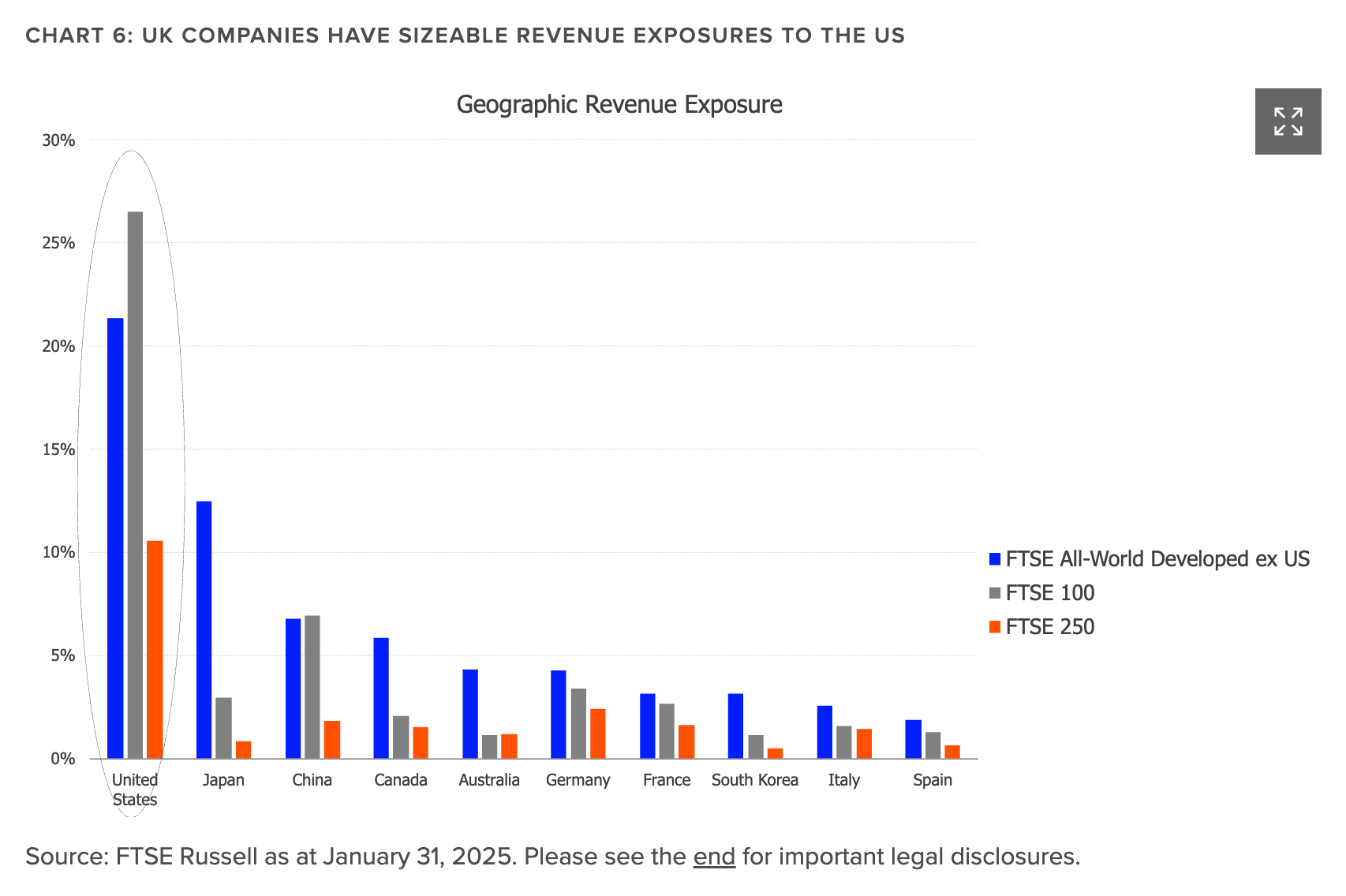

Take the United Kingdom as one example. The London Stock Exchange Group suggests that in 2025, the FTSE 1001 (the index tracking the biggest UK stocks) “derives nearly 30% of its revenue from the United States, far outstripping contributions from other regions such as Japan and China”, highlighting the “critical role of the US economy in driving earnings for UK-listed companies”. You never truly escape FX risk.

If a tree falls in the forest, does it make a sound? Of course it does. While FX can be out of sight, out of mind, it’s still there. The ramifications still trickle their way into the market pricing machine’s outlook on share prices. I am certain that even the staunchest domestic investors will have read through earnings calls and filings and recall disclosures of figures presented in constant currency, commentary on FX headwinds, various footnotes on hedging gains and losses, and so on. Yet because this seldom amounts to more than a few percentage points of difference in reported figures and does not bear a direct cost to your P/L, it’s commonly glanced over and forgotten about.

It’s one of those things that only alarms you when there is cause for alarm. I’ll admit that it’s something I seldom think about too deeply. This is despite having only ~30% of my invested assets allocated to domestic equities. The remainder is invested across equities listed in the United States (USD) and Europe (EUR), relatively stable currency pairs during my lifetime as an investor (which isn’t a long timeline).

Recently, I have been studying a few businesses in Japan. Two examples are Fast Retailing and Kikkoman Corporation.

Fast Retailing (9983), owners of the splendid Uniqlo brand, which I think highly of. Their combination of high-quality materials at an affordable price point is unrivalled. An offering particularly relevant in a world suffering from the ramifications of high inflation. Their stores are immensely popular wherever I happen to find them. In the small island of Singapore, there are 29 stores of all shapes and sizes. During a recent trip in December, I must have visited 6 of them, and they were constantly packed with customers. I had a similar experience when travelling in Thailand in early 2025, which is home to 72 stores. Even in India, where I happen to spend a lot of time, Uniqlo is growing a presence here. In Scotland, they opened a large store a few years back in the capital city, in a second-rate location on the former shopping hub known as Princes Street. Even today, it welcomes droves of customers like its opening weekend.

Uniqlo is a household name across Japan, China, and the rest of Southeast Asia. In what sounds like a tantalising opportunity, the brand is relatively unknown in the West, with just over 100 stores in North America and 91 in Europe. In the last 12 months, Uniqlo’s store count has grown by 18% and 11% in North America and Europe, respectively. The company’s revenue and profits have been growing like a weed, but so too has the valuation.

I stuck it in the “unsure” pile with the intention of coming back to it in the future, and moved on. I liked the business, was excited about the reinvestment runway, but couldn’t get comfortable with the valuation.

Kikkoman Corporation (2801) is the manufacturer of the world’s most well-known soy sauce, Kikkoman, as well as a host of other consumer products like seasonings and milk products. A different animal from Fast Retailing. In comparison, Kikkoman is more of a stable, steady growth, income-bearing, stalwart type of holding. I don’t subscribe to labels related to investment style. I optimise for businesses I can understand and that I think will surpass my threshold for attractive returns. So long as I think they can overcome that hurdle, I don’t personally care if the CAGR ends up being 14% or 45%. Obviously, the latter is better, but I often see DIY investors fall victim to seeking only outsized returns and end up being long a single factor.

I saw potential in the business, and the valuation was more palatable. But I couldn’t escape the feeling that I was making a macro call as well as a fundamental decision. My expectation of the potential future returns of Kikkoman was closer to the lower end of my threshold than Fast Retailing (at a more attractive valuation). It was at this point that I started to think about the impact of FX.

With a high-flying growth style stock like Fast Retailing, a valid entry point could prove to be forgiving when total returns are considered. However, if something is expected to compound at, say, anywhere between 8% and 12%, then a few hundred basis points of FX impact either way can have a more visceral impact. Suppose that domestic investors in Kikkoman over the past decade would have earned a modest 7.7% CAGR with dividends. Not catastrophic by any means, but not fantastic. An investor from the United Kingdom, however, would have earned a 5.2% CAGR after the FX drag had been factored in.

Consider that the UK-listed S&P 500 index put up a 16% CAGR over the same period… Ultimately, Kikkoman was not for me. Yet I was interested in the self-reflection that I found myself thinking about FX considerably more than I usually do. I was not solely making an investment decision on fundamental grounds. I would also be making a macro call that the Yen would (preferably) strengthen post acquisition.

The Yen has weakened relative to the GBP in recent years. In fact, it’s the weakest it has been since 2008. The ideal case would be that the Yen strengthened until the time I come to sell, meaning I receive more GBP per unit of JPY sold. In my naive monkey brain, this seemed like a more likely outcome and would be a welcome tailwind should I own the stock for a period of five to ten years.

Line went up for long time, so now should go down for long time.

I’d hardly call myself a proficient fundamental investor, let alone a foreign exchange oracle. I would also have to contend with the state of the Japanese economy and its influence on exchange rates. I find the prospect of conviction in the face of volatile FX rates is harder to stomach than fundamental volatility. I am more confident in riding a storm when it comes to my understanding of whether the impacts on the business are temporary or structural. I am significantly less confident (or perhaps less deluded in my ability) when it comes to understanding if FX rates are going to be a short-term headwind or a decade-long handicap.

I noticed myself agonising over a factor I seldom considered at great length when purchasing US or European stocks. Yet, even for these established currency pairs, there have been periods of significant tide changes. Only, I am too young and too naive to appreciate them.

As a teenager, I recall hearing the adults in the room recall when you could get two US Dollars for a Pound. In my lifetime, the duration that I have been cognisant of units of exchange, at least, the going rate has oscillated between $1.20 to $1.45. History shows that the relationship between the US Dollar and the Great British Pound hasn’t always been so boring. There have been various periods across the last five decades, when one side of the pair has strengthened against the other by orders of magnitude ranging between 30% and 60%.

The United States is arguably the most attractive financial market in the world. It just so happens I was born in a country and at a time which has been characterised by a relatively stable foreign exchange with the United States. This, I believe, has created a sense of complacency in myself, and I suspect others, with regard to currency impacts. Perhaps it’s a sign of maturity that after a decade of investing, I begin to consider this risk that feels out of sight but could one day be front of mind. Perhaps it’s because this month I finished reading ‘The Asian Financial Crisis’ by Russell Napier, which discusses the intensity of currency flows during the 1997 crisis. Perhaps it’s a byproduct of compounding.

When I was younger, and my portfolio was smaller, I noticed the FX impacts on my P/L statement. But they were so small I didn’t think much about them. These days, the aggregate FX impact of my US and European holdings is something I pay a lot more attention to because the numbers are no longer so insignificant.

To provide an example, I have owned Alphabet since July 2022. That initial lot is now up 208% from its purchase price. However, if I were to sell it today, it would amount to a return of 173% after accounting for the FX drag. That’s a 35% reduction in performance. Comparatively, I have owned Apple since September 2018. The raw total return is 343%, with just a 10% reduction in return thanks to FX. While a few holdings are boasting FX gains, it nets out to an aggregate loss on the FX side of things for me. As the portfolio has grown, so too has the implicit cost of conducting affairs in foreign stocks. Not that I actively do anything about it, mind you.

The last year or two has been marked by a weakening US Dollar. Amongst some of the world’s most liquid currencies, the last year has been a handicap for foreign investors invested in US stocks. The US Dollar Index (DXY), which measures the performance of the USD relative to the world’s largest currencies, has declined2 by almost 10% in the last 12 months.

What does this mean for foreign investors? Let’s use an illustration from my own portfolio. Take the UK equivalent of the S&P 500 ETF, VUSA, as one example. While the US counterpart (SPY) has put up 18.3% total returns over the last 12 months, UK investors in VUSA have only seen 7.9% returns thanks to a stuttering Dollar. Thankfully for me, I also invest in the domestic market. The UK’s FTSE 100 ETF, VUKE, has returned an impressive 26.5% over the same period. Just don’t pull back the chart history any further…

The irony in my reflections is not lost on me. As it were, I have been making macro bets all along. Recency bias, stability bias, whatever you wish to call it, has created an illusion of safety for me. As Hyman Minsky famously said, “Stability is destabilising". The longer nothing bad happens, the more comfortable people become with risk, and the more risk people take.

Only when venturing into unfamiliar terrain (Japan, in this case) did, for me anyway, the same risk present itself more noticeably. As though I am now in earshot of the tree that falls in the forest.

To disappoint anyone reading, there is no strong meaning or takeaway behind this note. Perhaps you can infer your own. I write primarily to transfer thoughts onto paper in the hope that I can reflect on them with a clear mind. It is by airing my ignorances and naivety that I compel myself to do something about them and learn.

Thanks for reading,

Conor

24-FEB-2025, UK equities − a haven for income and value

DXY 1Y Return

A question worth pondering.

Why do most FX charts, such as your Koyfin chart of the pound/dollar, begin in ~1973?

It is possible, Conor, you selected the time period. But that span of time is rather common for "long-term" FX charts. The answer, I believe, will tickle your intellectual curiosity.

Excellent as always.