The 200 Year Old Champagne Maison You've Never Heard Of

(FRA:LPE) Laurent Perrier has doubled EPS over the last six years under a new premiumisation strategy

A Global Stage Shared By Few

If I ask one hundred investors to name a few public companies in the alcohol industry, the usual suspects will surface. Companies like Anheuser-Busch (Budweiser, Stella Artois, Estrella), Diageo (Johnie Walker, Guinness, Captain Morgan), Heineken (Amstel, Heineken, Red Stripe), Constellation Brands (Modelo, High West, Corona), LMVH (Hennesy, Moët & Chandon, Glenmorangie) and Pernod Ricard (Jameson, Absolut, Malibu). Bonus points to those who would have said Campari Group (Aperol, Campari, Frangelico) because they own some of my personal favourites. They are home to the world’s most favoured beers, wines, and spirits.

Of those hundred investors, I wager fewer than four would have replied Laurent Perrier. There are a few hundred Champagne Maisons throughout the Champagne region of France; for the meme connoisseurs amongst us, only wines produced in this region may be labelled and sold with this prestigious title. Laurent Perrier, with its rich history stretching back to the early 1800s, is one of those Maisons, making it a rarity. Rarer still, it’s one of the few traded on public markets (FRA:LPE).

Champagne Heritage

Producing champagnes since 1812, Laurent Perrier is the company’s flagship brand; accountable for 44% of group revenues1. They are particularly well-known for their cuvée and offer a limited range of core and speciality wines, priced towards the higher end of the market. In the champagne world, the term cuvée has many meanings. In the context of this article, it’s enough to know that a cuvée indicates the wine is a blend of grapes. It’s also a designation which refers to the first-pressed juice for the wine; which is considered the most potent, flavoursome, and highest quality of the batch.

Having sampled a few of these champagnes, I can attest to their quality as a layperson. The Cuvée Rosé is particularly great. You’ll find that a bottle from their classic collection will cost anywhere from ~$65 for their standard La Cuvée to ~$110 for the Cuvée Rosé. Speciality champagnes, such as their Alexandra Rosé Millésime, will go for $500 to $1,000 depending on the vintage. Coming in at ~$250, the Siécle Grande Cuvée N.26 was awarded Wine of the Year 2023 by James Suckling; beating out 39,000 others. Receiving the highest score (100/100), it was described as being “electric on the palate” with a “freshness and balance that draws you back”.

Brands like Moët & Chandon, Dom Pérignon, and Bollinger enjoy widespread recognition. But Laurent Perrier stands tall amongst the world’s most popular champagnes, producing ~7 million bottles each year. As we will come to learn, production volume isn’t everything. It’s estimated that Laurent Perrier controls a worldwide market share of ~3.5% to 4%.

As a group, Laurent Perrier is exclusively focused on Champagne and owns a total of four brands. While not as renowned as the namesake label, they also own Delamotte (1760), Champagne de Castellane (1895), and Champagne Salon (1920).

Keep It In The Family

Laurent Perrier was born in Tours-sur-Marne, France, the heart of the Champagne country. Cask maker and bottler, Alphonse Pierlot, founded the business in 1812. After his passing, and with no descendants, the business was inherited by his cellar master, Eugène Laurent. It wasn’t until 1887 when the newly widowed Mathilde Emilie Perrier took ownership that the company would bear the name Veuve Laurent-Perrier. She would find moderate success and by the time the First World War came, Laurent Perrier had become an international brand; marketing itself to UK audiences. In 1925, Mathilde passed away and left the company to her daughter who would sell the business in 1939.

The acquirer was one Mary-Louise Lanson de Nonancourt. Her acquisition of Laurent Perrier was the inception of family ownership that would continue for the next 85 years and is still ongoing. Mary-Lousie’s youngest son, Bernard de Nonancourt, would inherit the business in 1949 and become a pivotal figure in the business’s history.

“After returning from the war, Bernard de Nonancourt completed a demanding apprenticeship in the vineyards before becoming CEO at the age of just 28. At the time, the company employed around twenty people and sold 80,000 bottles. Under his leadership, Laurent‑Perrier became a true innovator in Champagne in just 40 years. Fascinated by innovation, attached to the traditions of the Champagne region and the quality of its people and wines, Bernard de Nonancourt created the Laurent‑Perrier style - freshness, elegance, purity - and developed a unique range of champagnes that were exported worldwide to more than 160 countries”.

The company’s acquisitive exploits would occur under Bernard. A majority stake was acquired in Champagne de Castellane in the early 1980s, resulting in a full acquisition years later. Delamotte was acquired in 1988, followed by Champagne Salon one year later. In 1999, the company floated on the Paris Stock Exchange and created a management structure that introduced Bernard’s daughters, Alexandra Pereyre and Stéphanie Meneux de Nonancourt. Following his death in 2012, his children continue to run the business to this day. Anchored in its homeland, France, the group operates 6 subsidiaries throughout Europe with one in the United States2 and partners with independent distributors in more than 140 countries.

Owner Mentality

Throughout the De Nonancourt’s tenure, the family has controlled the majority of the ownership and voting rights. At present, they own ~65% of the outstanding shares and ~78% of the voting rights. Since 2000, the outstanding sharecount3 has never deviated more than 2%. By now you’ve probably guessed Laurent Perrier is a fairly illiquid stock. You’d be right. Throughout the last decade, Laurent Perrier’s market cap has shifted between €350 million to €830 million. On an average day, the stock will trade 820 shares or €65,900 in notional value. Nick Train, of Lindsell Train, commented on the difficulty of accumulating a position in Laurent Perrier during their 2023 annual report:

“In fact, our only activity was to add to our most recent position, Laurent Perrier. This is now getting on for a 2% holding and we look to build it further, when shares come available, which is infrequently”.

Lindsell owns less than a percentage of the business. First Eagle Investments (an investment advisory) is the largest outside owner, at ~9% of outstanding shares and ~5% of voting rights. In a 2019 memo, First Eagle commented on Laurent Perrier in a segment titled the “Search for Quality”.

“Another example of an old family-owned business is Laurent-Perrier a Champagne maison founded in 1812 and controlled by the De Nonancourt family, which has been running the company for three generations and currently owns 61% of it. With its supply structurally limited by French law that defines the geographic area in which it can be produced, Champagne is a scarce asset, and the vast majority of both the wine and the grapes needed to produce it are in the hands of large maisons like Laurent-Perrier. While its Champagne brands—most notably Laurent-Perrier but also Salon, De Castellane and Delamotte—are very valuable, Laurent-Perrier also controls certain impossible-to-replicate assets in the form of its vineyards and other prime real estate and its large inventory of aging bottles”.

Constrained supply is a beautiful thing for luxury businesses. Only so much Champagne can be produced in the region each year. It’s heavily regulated and the barriers to entry are high. The average Champagne Maison will produce ~20% of its grape yield from their own vineyards each season. Contrary to peers, Laurent Perrier produces only 10% of its grape requirements from owned vineyards in a given year. They say this is because they “never believed that the purchase and operation of vineyards should be its core business” and instead favour agreements with a range of wine growers. This has allowed them to be flexible and keep fixed costs low. Areas they can exercise some control is in their reserve inventory management. Nonetheless, a myriad of external factors influence yields such as weather, contracts, and regulation. Not to mention the fact Champagne of this quality must undergo lengthy ageing processes, at times up to 15 years.

Champagne’s scarcity and the muscle of pricing power make it a natural luxury product. Scarcity is great Laurent Perrier, but what about shareholders? With so few shares traded, it requires an investor who is either (a) patient or (b) certain of a particularly potent catalyst or liquidity-inducing event. For the patient investor, you are investing alongside the family which has owned the business for what is now approaching a century. Companies with such ownership tend to ignore the quarterly posturing and fanfare of appealing to analysts. Instead, they make long-term decisions, which isn’t a luxury afforded to most management teams. Of course, this has its downsides too. While a family-owning 78% of the voting rights are unlikely to be distracted by quarterly minutiae, they are equally unlikely to be influenced by warranted activism or shareholder unrest. It’s their damn business after all. In Laurent Perrier’s case, there has been no precedent for concern.

Two Distinct Stages

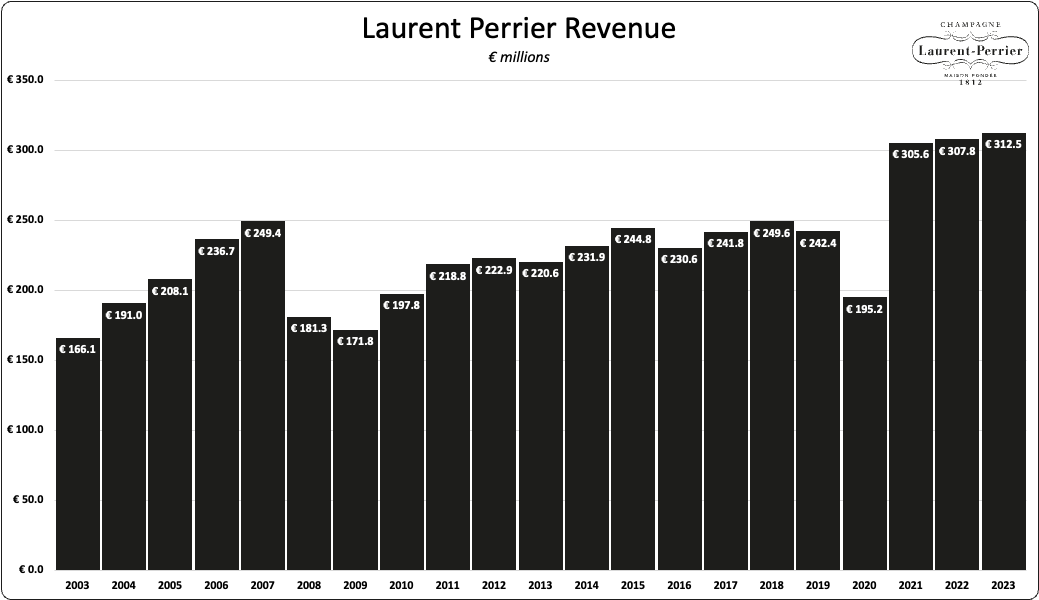

Looking backwards can be a deceitful practice for an investor. We do so for a fuller understanding of the backstory and history of the business. We want to see how management teams behave under various regimes and cycles. How the products hold up over time. Laurent Perrier struggled following the great financial crisis of 2008. Revenues took a 25% haircut and wouldn’t recover for ten years. Last week, Laurent Perrier reported an all-time high of €312.5 million in group revenue for 2023.

When dreams are smashed, expectations are reset. Following a plunge in demand for champagne in the wake of the crisis, Laurent Perrier’s stock price bottomed out at ~€30 per share4in the first quarter of 2009. From there it has gone on to produce ~9.5% compounded annual returns. Not too shabby. It’s more accurate to look at these two distinct stages in the company’s history as one embodied by steady growth that was crushed by a global crisis and the other as the long-winded recovery. Following the most recent external shock, the 2020 pandemic, Laurent Perrier recovered much faster. Why?

The most accurate answer is outside of the remit of this article. It’s enough to say this shock was different and inflicted pressure on consumers’ finances and taste for luxury that was more ephemeral. It was fierce, unprecedented, and uncertain. Unemployment rocketed, stock markets cratered, and the gauges for global supply and demand aggressively recalibrated several times to reflect the continuously evolving reality we found ourselves in; the effects of which are still reverberating through the economy. But I suspect that in years to come, people will look back on this time and feel that it disappeared as suddenly as it arrived. Stock markets had recovered by the Fall, unemployment soon retreated to multi-decade lows again, and following a boom for e-commerce companies came the inevitable recovery of the out-of-favour physically-presenced businesses. Governments were quick to step in and support the consumer, who was looking for ways to occupy their time as they remained indoors for the better part of two years (Champagne anyone?).

Pricing Power

Laurent Perrier has proven to be resilient in the face of a crisis; the management team now has a few under their belt. But this recent chapter of recovery had other dynamics at play. Following the great financial crisis, there was a bout of inflation. Rates varied, but across the United States and Europe, they would peak at 5.6% and 4.1%, respectively, before disinflation and even a brief period of deflation in 20095. Rates wouldn’t cross 4% again until 2021; and boy did they cross 4%. Inflation has since cooled but climbed to as high as 10.6% and 9.1% across the US and Europe throughout 2022 and 2023.

During this inflationary phase, most companies began to pass on price increases to consumers as a way of offsetting costs. Laurent Perrier was no different. While it’s always been a part of their strategy to inflate their prices over time, much like any luxury business, the last few years have been particularly notable. In the years 2022 and 2023, Laurent Perrier saw champagne revenues grow by 3.1% and 0.5% while volumes fell by 7.4% and 12.4% in consecutive years.

Over the period, the price mix effect was 9.5% and 13.0%; considerably higher than usual. In other words, Laurent Perrier has been maintaining (modestly growing, even) Champagne revenues while aggressively pricing their offerings upmarket. Operating profits have benefited greatly. From 2018 to 2023 Laurent Perrier has grown operating profits by 130%, margins have expanded from 16.6% to 31.3% for Champagne and they grew earnings per share by 176%. Net income margins, currently at 20% of 2023 revenues, are at all-time highs too.

You may ask how sustainable this is.

It’s likely the elevated price mix will float back down to mid-single digits in coming years, but this wasn’t a strategy conducted in the frenzy of a crisis. Laurent Perrier’s Value Policy has been in place for several years before the pandemic. The policy saw the management team explicitly focus on positioning their premium cuvées within the higher end of the market. They felt they were leaving money on the table. Paraphrasing from a couple of the last annual reports: