Placing Your Bets In The UK Gambling Industry

Why Regulation is Causing UK Gambling Companies to Look to the States

Hey, you are reading Investment Talk. If you enjoy today’s article, feel free to share it, or become a supporter, it helps a lot. Now let’s begin.

What are the Odds?

If there is something Brits are great at, it’s pissing their residual income down the drain in the form of sports betting. The Americans, who are now witnessing a wave of online gambling following legislative changes, gambled $93.2 billion on sports last year1 netting the industry $7.5 billion in gross gaming revenues (+73% from 2021). While the US is certainly larger when factoring in the total gambling market, it won’t be long before they overtake the UK in online sports betting. In the States, in-person gambling continues to be the backbone of the industry but online gambling represents a growing share.

The UK, a mature online gambling market, has already borne witness to the erosion of in-person bookies. In the last decade, the number of physical betting shops in the UK has fallen by a third; with ~6.2k remaining. As the brick-bound relics of a past generation struggled to keep up with modern times, the industry consolidated into an oligopoly that, between them, own an impressive roster of brands. While the growth of online betting remains fruitful in the UK, investor optimism is led by both the scale of these companies’ online platforms and their progress in establishing a presence on the newly fertile soil of America.

Reforms, Baby

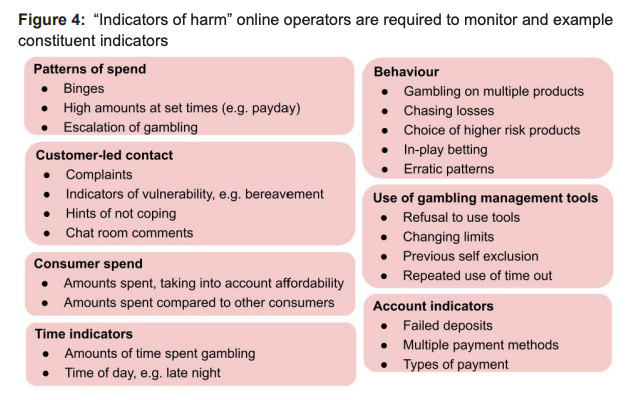

This year, the UK’s gambling industry got a wake-up call. Being a gambling business in the UK has become progressively harder as the government looks to clamp down on sports betting by protecting problemed gamblers. While operators’ approaches to counteracting this vary, the strengthened Gambling Commission rules which came into force in September 2022 and February 2023 have clarified operator responsibilities around customer interaction and have mandated consistency across the sector. The Government’s 2023 paper, High Stakes: Gambling Reform for the Digital Age, lays out these rules in an effort to prevent gambling-related harms. According to a 2021 parliamentary report2, 60% of industry profits come from the 5% of users who are either problem gamblers or at risk of becoming so. Protecting these vulnerable addicts will surely syphon off the fat-cat’s best customers. The below table illustrates seven relevant categories of “indicators of harm” that all operators must monitor from the moment an account is opened. Operators must tailor the action they take based on these behavioural indicators.

Specific proposals from the paper include, but are not limited to:

• Introducing stake limits for online slots, of between £2 and £15 per spin; with harshes stake limits for 18-24 year olds.

• More prescriptive rules on when online operators must check customers’ financial circumstances for signs their losses are harmful. The paper suggests this may start when net losses exceed £125 within a month or £500 in a year.

• For higher net worth gamblers, the paper suggests a welfare check after £1,000 to £2,000 net loss within a 3 month period.

• Making online games safer by design by reviewing game speeds and removing features which exacerbate risks.

• Commission to consult on making data sharing between online operators on high-risk customers mandatory for collaborative harm prevention.

• Ensuring that incentives like bonuses and free bets are constructed in a socially responsible manner that does not exacerbate the risk of harm.

• Strengthen informational messaging including on the risks associated with gambling.

• Removing high risk features of online game design. The wheels are already in motion. Shortly after the paper was published the Premier League, the nation’s largest gambling enabler, agreed to end front-of-shirt sponsorship deals by gambling firms3.

"A stone was dropped in the water a long time ago, and we're only seeing the ripples now”.

While the paper targets problemed gamblers, the impact of betting reforms will be felt further afield; as Robin Hardy recently pointed out in the Investor’s Chronicle:

“While primarily targeting problem gamblers, [the whitepaper] will inevitably impact all players. Stake limits and data sharing could materially reduce total revenues in UK online gaming as problem/addicted players have been responsible for a material amount of the industry’s total revenues”.

Whether the reforms help troubled gamblers or not; the direction the government is taking will make it much harder for companies to exploit these consumers. Meanwhile, over the pond, the gold rush is just starting, and bureaucrats are too busy loading up their wheelbarrows to care about second-order effects. Therefore, exposure to the domestic market is likely to dismay prospective investors. The value that these investors are willing to place on those companies will also be lower. So who is there to choose from?

The Four Horseman

Consolidation means only a handful of gambling companies are listed in the UK, but they cover a lot of ground. In order of market capitalisation, they are Flutter Entertainment (FLTR), Entain (ENT), 888 Holdings (888), and Rank Group (RNK).

Flutter Entertainment (FLTR)

Flutter Entertainment, the lovechild of a merger between Paddy Power and Betfair, is by far and large the biggest player in this basket, with a market cap of £27 billion. Internationally diversified, Flutter’s revenue is primarily based in the US (34% of 2022 revenue) and they have sizeable exposure to the UK (28%), and Australia (16%), as well as another 22% of sales originating from overseas markets including India and China. Thanks to their active role in the M&A market, Flutter is home to an array of brands such as Paddy Power, Tombola, FanDuel, SkyBet, Sportsbet, Pokerstars, Betfair, Junglee, FoxBet, Junglee Games, Abjarabet, and TVG.

Flutter Entertainment, Recent M&A

2021

• Sisal, $2.2b

• Tombola, $540m

• Singular, $45m

• Oddschecker GM, $215m

• Junglee Games, $66m

2020

• FanDuel, $4.2b

2019

• The Stars Group, $12.3b

Data is pulled from S&P's Capital IQA couple of things that Flutter has going for them. First, they have a limited physical presence in the UK, with slightly more than 600 Paddy Power betting shops across the country. Second, and most importantly, the US portion of their business is driving growth thanks to the explosion in online gambling. To put the appropriate perspective on just how fast it's growing; by the end of 2020, the UK and US businesses brought in revenues of £1.75 billion and £673 million respectively. By the end of 2022, the UK and US businesses had grown 22% and 287%; bringing in £2.14 billion and £2.6 billion respectively. By tapping into a rich new market, Flutter’s average monthly players increased 26% last year, to 10.2 million. In the first quarter of 2023, the company added a further 2.1 million players. First quarter revenue for the company (£2.4 billion) expanded by 54% thanks to a 92% increase in US revenues; including a 147% jump in sportsbook revenue.

This aggressive acquisitive behaviour, and well-timed pivot, allowed the group to avoid a covid-induced glut in earnings. EBITDA for 2022 (£1.05 billion), sits more than 2x above 2019 levels and is expected to more than double by the end of 20244. At present, Flutter’s combined online market share in the US surpasses 22%, with a 50% share of sports betting and a 21% share of the iGaming market. Comparatively, the company holds a 28% online market share in the UK and controls 48% of the Australian market. The UK government’s stance on gambler protection is a noble one, but thankfully for Flutter, management has expressed it won’t come with grave consequences. CEO, Peter Jackson, remarked during the latest earnings call that the framework set forth by the whitepaper is expected to have as little as “£25 million to £50 million EBITDA impact, with half in 2024 and the rest in 2025, largely as a result of the proactive actions we've already taken”. While management remarked that “In the UK, the publication of the White Paper has vindicated the proactive actions we have taken” to further gambler safety, the underlying message is this; we are no longer focussed on the UK. Flutter has already begun taking steps to distance itself from the UK, with a US listing expected sometime towards the end of 2023; adding that “over the coming months, we'll be considering our approach with respect to our existing Euronext and London listings”. While the UK may be a cheaper alternative to listing in the US, there is no denying the appeal of the States. Valuations tend to be higher, liquidity is greater, and there is less scrutiny over executive compensation; I could go on.

Flutter’s US intentions are clear, and their progress on that front is impressive. It, therefore, comes as no surprise that the market has slapped the heftiest premium on the shares. Trading at 39x forward earnings, Flutter commands a considerable premium over the rest of the basket. By 2024, consensus estimates suggest Flutter will be earning £10.6 billion in revenues (+38%), £6.7 billion in gross profit (+48%), and will surpass £1 billion in net income (+208%). They say you have to pay up for growth, and it seems that’s what investors have been doing. More importantly, the US market is still in its infancy. The market for Sports betting and iGaming is estimated to be worth $9 billion as of mid-2022; a figure which is expected to grow to more than $40 billion by the end of the decade.

Any concerns about market saturation or the company not having attractive avenues for reinvestment will be moot for the coming decade. For investors looking to gain exposure to the US through a UK vehicle, I think Flutter, valuation aside, is the most compelling option. The current valuation may already be soaking up much of that optimism, however, so finding the right price is up to the individual.

Entain (ENT)

Entrain, the second largest of the group, is an interesting proposition. While it has less than a third of Flutter’s market cap, its trailing gross profit (£3.5 billion) sits only a fifth lower with trailing margins of 82% compared to Flutter’s 59%.

While the discrepancy may appear attractive at first glance, Flutter’s margins have come at the expense of their aggressive US and online expansion. Entain’s progress in this area has been less spectacular. While Entain does have a US footprint through a joint venture with MGM Resorts (more on that shortly), the acquisition of Ladbrokes Coral Group in 2018 absorbed a considerable footprint in physical UK betting shops; more than 2,700. As such, Entain’s share of revenue coming from the UK (27%) is their largest, followed by the US (15%) and Australia (14%). Knowing this, it calls comes down to the rating investors give to Entrain’s operational profile. Because they are so exposed to the UK, the whitepaper will have a more profound effect on their future earnings; limiting growth potential.

Entain Plc, Recent M&A

2023

• STS Holding, $943m

• 365 Scores Ltd, $160m

• Tidal Gaming NZ, $8m

2022

• Super Sport, $713m

• Bet BV, $885m

• Totoletek, $7m

• Avid International, $235m

2021

• Enlabs, $425m

2018

• Ladbrokes Coral Group, $6.8b

Data is pulled from S&P's Capital IQTo break ground in the US, Entain partnered with industry veteran MGM Resorts in a joint venture called BetMGM; which is currently live in 29 jurisdictions, with access to >50% of the US population. The partnership is a bright spot in Entain’s business; net gaming revenue from BetMGM surpassed $1.4 billion in 2022 (+71% YoY) and is expected to be EBITDA positive by the second half of 2023. Meanwhile, Entain’s core online segment saw revenues decline 2% YoY; to £3.1 billion. There had been speculation over an Entain acquisition after the company announced, in Q4 2022, that they would cease to invest in BetMGM after it moved into profitability; thereafter providing ongoing operational support from technology to product. However, MGM’s CEO put those rumours to bed swiftly.