Europe's Magnificent Eleven

Evidence that the American and European markets have become increasingly top-heavy

I was today-years-old when I learned that Europe has its own version of the Magnificent 7; the basket of giga-cap US tech companies comprised of Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla.

The GRANOLAS

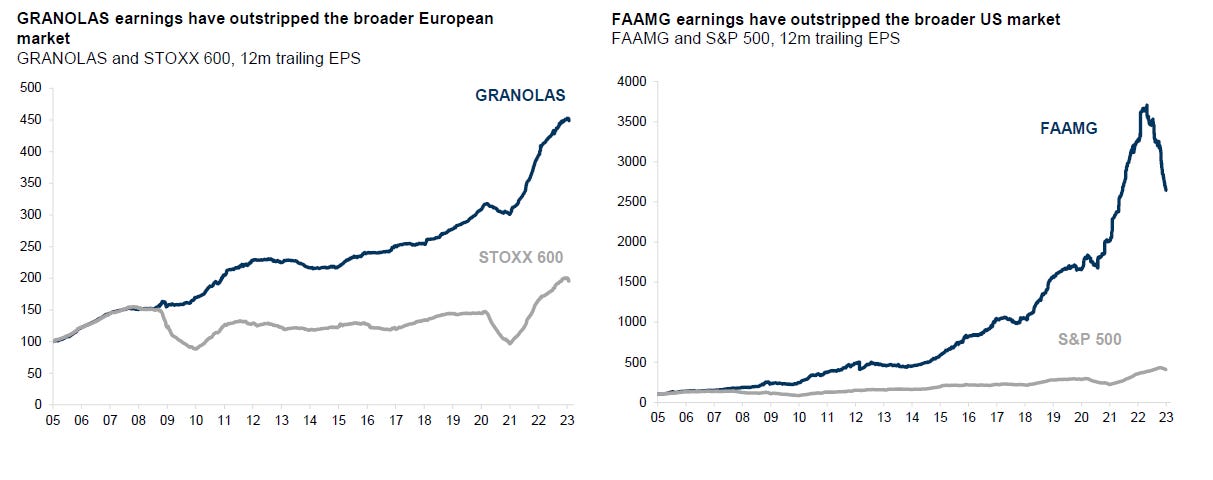

Dubbed the “Granolas” by Goldman Sachs in 2020, this basket was chosen because it echoed themes present amongst the Mag 7 (back then it was just “FAAMG”). Namely, they were market leaders in the STOXX 600 Europe Index, they had grown to become an increasingly larger share of the market, and their earnings had far outpaced the broader index.

Like the Mag 7, the Granolas represented the biggest and best companies across their region. This European line-up included 11 companies across 6 countries; LVMH (MC), Sanofi (SAN), and L’Oreal (OR) from France, Novartis (NOVN), Nestle (NESN), and Roche Holding (ROG) from Switzerland, GSK (GSK) and AstraZeneca (AZN) representing the United Kingdom, ASML Holding (ASML) the semiconductor business from Holland, SAP SE (SAP) from Germany, and Denmark’s Novo Nordisk (NOVOB). According to the Financial Times1, this group have accounted for ~50% of the gains in the Stoxx 600 Europe index over the last 12 months, and half of all M&A activity. The elevensome is up ~9% so far this year, ahead of the Stoxx 600’s 3.5%.

Are they stronger performers?

The Down Jones reported2 earlier this month that “this grouping of stocks has actually kept up with the Magnificent Seven, and with a lot less risk”. Naturally, I wanted to explore whether or not that’s true. As I perused the public discourse on the Granolas I was confused about what the fuss was about. The performance relative to the Magnificent Seven is hardly something to write home about. Since the beginning of 2022, the Granolas are +28% compared to the Magnificent Seven’s +142%. When you look at the two baskets from 2021 onwards, the gap between performance is narrower (Mag 7 +96.4% vs Granolas +69.4%) but the Granolas generated returns with considerably lower downside.

Throughout this period the Granolas have reported annualised returns of 18.3% compared to the Magnificent Seven’s 24.8%. But the former’s impressive performance didn’t come without stress. If you owned the Magnificent Seven over this period, you would have endured a 50% drawdown that started in late 2021 and wouldn’t fully retrace until the summer of 2023. Meanwhile, the Granolas would not have suffered a drawdown of more than 15%.

This is presumably because the Granolas are made up of different atoms. The two baskets share some commonality in their mutual exposure to information technology and consumer discretionary sectors, but as far as industrial exposure is concerned, the distinction is unmistakable. The Granolas have the majority of their exposure in the pharmaceuticals industry across companies like Novo Nordisk, GSK, Novartis, Sanofi, AstraZeneca, and Roche Holding. Unlike the Mag 7, the Granolas lack the presence of any major media or technology companies; those which were hit especially hard at points in the last three years.

While the performance is not as reminiscent of the Magnificent Seven, the outperformance relative to their respective benchmark certainly is. Perhaps this is where investors are finding commonalities.

Are they cheaper?

Morningstar makes the case that the Granolas are “profitable and cheaper” than their American cousins. This was a common thread in the coverage I read. Optically, that is true for the most part. This market scatter shows the current forward sales and earnings multiples across each basket. You’ll notice that most of the Granolas trade at more accommodating multiples.

Taking a deeper look, I constructed a table to outline the margin profile of each company (market caps are converted to USD for comparative reasons). What you will notice is that the Magnificent Seven are, on average, gigantic. The smallest constituent, Tesla, weighs in at $635 billion in market cap. That’s larger than any of the European companies and more than twice as large as the average. Together, the Magnificent Seven have an average market cap of ~$1.89 trillion compared to the European’s $270 billion.

But Morningstar is right; these companies are relatively cheap and profitable. More profitable than the Magnificent Seven on a common-size basis. The average gross margin amongst the Granolas is just shy of 70% compared to 56% in the Mag 7. However, that’s where the flattery ends. On average, the Magnificent Seven have superior operating, net, and free cash flow margins. What's more, Tesla’s lower-margin auto manufacturing business brings the basket’s gross margin down by ~600bps. They may trade at higher multiples, but the average 5Y CAGR amongst the Mag 7 is more than double that of the Granolas.