Warren Buffett: The Investor's Investor, 1979

A 48 Year Old Buffett Discusses Early Life, His Investment Process, and How It Has Changed Over the Years Through Various Influences

In 1979 a man named John Train profiled a young(er) Warren Buffett, aged 48 at the time, in a publication called Financial World to promote his upcoming book; The Money Masters, which would publish the following year. Spanning a 5-page spread in the newspaper, the conversation that Train had with Buffett covers his coming of age as a young adult, his relationship with mentor Ben Graham, and flecks of how his investment process transformed over the years. Perhaps unsurprisingly, not a great deal has changed some four decades later.

I had noticed a few individuals sharing images of the article online but was unable to find a text-based copy of it anywhere, so took the liberty of transcribing it because I enjoyed it so greatly. I hope you enjoy it too.

Choice Quotes From the Article

• “The enormous advantage the independent investor has, Buffett says, is that he can stand at the plate and wait forever for the perfect pitch. If he wants it to come in exactly two inches above his navel and nowhere else, he can stand there indefinitely until an easy one is served up. Stock market investment is the only business of which that is true.”

• “Many times, though, the investment manager lets his advantage be turned into a disadvantage. Feeling obliged to remain active, he swings at far too many pitches, instead of holding off until he has an absolute conviction.”

• “The essence of Warren Buffett’s thinking is that the business world is divided into a tiny number of wonderful businesses - well worth investing in at a price - and a huge number of bad or mediocre businesses that are not attractive as long-term investments.”

• “Buffett understands the companies he owns stock in as businesses: living organisms, with hearts, lungs, bones, muscles, arteries and nervous systems. It is madness, he would say, for an investor buying stock to have anything else in mind other than the operating realities of the underlying business.”

Warren Buffett: The Investor's Investor

His message today: Stay clear of heavy industries

John Train, 1979

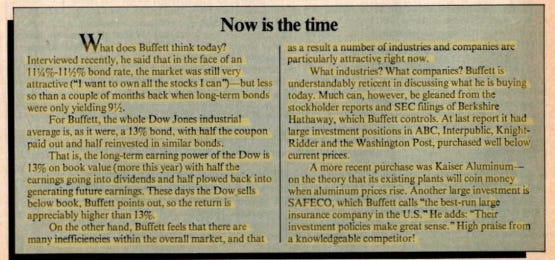

With the death of Benjamin Graham, the Maimonides of portfolio management, his disciple Warren Buffett of Omaha, Nebraska, may have succeeded to the title of the investor’s investor. He disbanded his troupe of less than a hundred clients, collected in a single pool called the Buffett Partnership, before his 40th birthday, to become a solo operator. Though he has written no textbooks, among investment professionals there is no more respected voice.

If you had put $10,000 in Buffett’s original investing partnership at inception in 1956, you would have collected about $300,000 by the time he dissolved it at the end of 1969. He has never had a down year, even in the severe bear markets of 1957, 1862, 1966, and 1969. That achievement stands alone in modern portfolio management. The portfolio of Buffett’s partnership was often too concentrated in a few issues - some not readily marketable - for an investment counsellor or fund manager, but not out of line with that what might be done by a conservative professional with his own money. Buffett now likes to own a dozen or so securities and characterises diversification as the “Noah’s Ark approach”: you buy two of everything in sight and end up with a zoo instead of a portfolio.

The essence of Warren Buffett’s thinking is that the business world is divided into a tiny number of wonderful businesses - well worth investing in at a price - and a huge number of bad or mediocre businesses that are not attractive as long-term investments. Most of the time most businesses are not worth what they are selling for, but on rare occasions, the wonderful businesses are almost given away. When that happens buy boldly, paying no attention to current gloomy economic and stock market forecasts.

The few businesses that Buffett thinks are worth owning often fall into the category he calls “gross profits royalty” companies, perhaps better called “gross revenues royalty” companies: TV stations, institutional advertising agencies, iron-ore landholding companies, [and] newspapers. Benefiting directly from the large capital investments of the companies they serve, they require little working capital to operate, and, in fact, pour off cash to their owners. The unfortunate capital-intensive producer - Chrysler, Monsanto or International Harvester - can’t bring its wares to its customers’ notice without paying tribute to the “royalty” holder: The Wall Street Journal, J. Walter Thompson, the local TV station, or all three. Other valid franchises Buffett likes include the large insurance brokerage agencies and some specialised ad hoc situations such as Sperry & Hutchinson Green Stamps.

Youthful Tycoon

Buffett’s office, on the top floor of a modern building about 15 minutes from the centre of Omaha, is clean and anonymous, with framed documents on the walls and a box of fudge on a table, to which Buffett helps himself from time to time. It’s delicious - made by a company he owns. A bookshelf on the wall holds, with other financial volumes, several editions of Graham and Dodd’s Security Analysis. Buffett, a genial, ruddy, muscular man with a wide, humorous mouth and an inquisitive expression behind his horn-rimmed spectacles, put his feet on the desk, poured himself a Pepsi Cola, and, in the somewhat toneless manner characteristic of Mid-westerners, cheerfully began to babble about what was on his mind. He speaks with a wry earnestness and gives an impression of complete intellectual honesty. His delivery is so casual, rapid, allusive, and clever that unless you pay attention a lot could slip by.

Says Buffett: “When I was a kid at Woodrow Wilson High School in Washington, another kid and I started the Wilson Coin-Operated Machine Co. I was 15 years old. We put reconditioned pinball machines in barber shops. In Washington, you were supposed to buy a tax stamp to be in the pinball machine business. I got the impression we were the only people who ever bought one. The first day we bought an old machine for $25 and put it out in a shop. When we came back that night it had $4 in it! I figured I had discovered the wheel. Eventually we were making $50 a week. I hadn’t dreamed life could be so good”.

Even before that, Buffett was well along in his career as a tycoon. At the age of 11, he made his debut as a market technician. Soon after, we find him in the business of retrieving and reselling golf balls and running several paper routes for the Washington Post. Delivery of papers accounted for most of his original stake of $9,000 with which he finished his college career. At 12, Warren became fond of handicapping horse races and compiled and sold a tip sheet called “Stable Boy Selection”. He found few aspects of commercial life beyond his grasp, even at that age. “I always knew I was going to be rich,” he has said.

The Graham Influence

As a boy, Buffett was fascinated by stock market technical analysis. He developed his own market indexes and the like but it all made no real sense to him. He discarded this approach in 1949, after reading The Intelligent Investor by Benjamin Graham while attending the University of Nebraska. The following year he went to Columbia University because both Graham and Dodd (of Security Analysis) were teaching there. Buffett noticed in Who’s Who that Ben Graham, was a director of Government Employees Insurance Co. (GEICO), which sold automobile insurance directly by mail, bypassing the brokers. He went down to the company’s office on a Saturday and pounded on the door. Eventually, a janitor opened up, and Buffett asked if there was anybody around he could talk to about the company. The janitor took him upstairs, where one man was in his office, L.A. Davidson, later chief executive officer. Buffett questioned him for five hours, then went away very excited about its stock.

After skimping to buy some shares, he discussed GEICO with two brokers who specialised in insurance issues: both pooh-poohed it since the company didn’t look cheap in their tables of insurance stock values. What the tables didn’t show was that the company was making 20% on its underwriting activities as against a normal margin of 5%. At that time the entire company was selling for less than $7 million in the market; later it went to a billion and became a Wall Street favourite. Some 25 years after Buffett made his initial investment in the company, mismanagement brought GEICO to the edge of bankruptcy. During that crisis, Buffett bought 15% of the company and thinks that it again has a bright future. Since Buffett believed in going to work for the smartest person available, on graduating from Columbia he offered his services to Graham for nothing. When Graham declined, Buffett went back to Omaha and entered his father’s stockbroking firm. Buffett kept in touch with Graham, however, sending him ideas in the hope of receiving stock exchange business.

Graham, in turn, was generous with his time and thoughts, and in 1954, he suggested that Buffett come to see him. Buffett went to New York and was hired to work for Graham-Newman Corp., where he spent two instructive years. Today he finds it hard to describe what he did there, but it must have included analysing hundreds of companies to see if they met Graham’s investment criteria. Ben Graham didn’t distinguish between franchises. He never would have been able to buy American Express during the salad oil scandal, or Disney, two of Buffett’s great coups. He did not believe in “qualitative” analysis - studying a company’s products, how it operates and its apparent future outlook. He never talked to managements. He believed in doing all his work by exhaustively studying figures generally available. This technique was immensely profitable for Graham and his investors, but did not really satisfy Buffett, who finds such mechanical investing all too similar to filling out an application for group life insurance. After his two years of apprenticeship in the workshop of the master, Buffett was glad to set forth into the great world as a master himself. For the second time he returned to Omaha, where he bought a roomy house - to which he has been adding sporadically ever since - on a wooded corner, and started on his own. In retrospect, one is not too surprised that, given such mental equipment, such fascination for the subject and such a thorough academic and practical preparation, Buffett should have done exceedingly well. Nobody, however, could have foreseen his record.

Buffett understands the companies he owns stock in as businesses: living organisms, with hearts, lungs, bones, muscles, arteries and nervous systems. It is madness, he would say, for an investor buying stock to have anything else in mind other than the operating realities of the underlying business. Buffett believes that those on Wall Street who talk of the stock trend or institutional sponsorship are ridiculous, combining laziness with ignorance, and compares them with astronomers, setting aside their telescopes to consult the astrology page. He thinks of a stock only as a fractional interest in a business and always begins by asking himself, “How much would I pay for all of this company? And on that basis, what will I pay for 1% of it?”. There are very few companies he considered interesting enough to buy at all, and even those he will look at only when they are very unpopular.

Buffett Partnership

In 1956, at the age of 25, Buffett started a family partnership with $100,000 in it, after a while adding all his own capital. As management, he received 25% of the profits above a 6% annual return on capital. As the partnership increased in value and his reputation spread, more money poured in. Homer Dodge, a physicist and former college president who excelled at picking stock-pickers, came to see Buffett, then 26, while on a canoe trip, with the canoe itself perched on top of the car. Long a friend and partner of Ben Graham, who had just retired, Dodge became Buffett’s first partner outside the family, simply writing out a check to join the partnership after a brief talk. Every year Buffett wrote his co-investors:

“I cannot promise results to partners, but I can and do promise this:

a. Our investments will be chosen on the basis of value, not popularity.

b. Our patterns of operations will attempt to reduce permanent capital loss (not short-term quotational loss) to a minimum”.

His stated goal was not absolute, but relative: to beat the Dow Jones by an average of 10 per cent per year. In general, he bought undervalued listed stocks, but also was unusually involved in merger arbitrage situations. Occasionally he bought a controlling interest in a public company or an entire private business on a negotiated basis. In 1965, for example, he took over Berkshire Hathaway in New Bedford Mass., a textile manufacturer with a long record of unprofitable operations, and installed new management. He now owns 47% of the company (former partners own another 35% or so) and it holds many of his other interests. He brought off perhaps his most spectacular transaction in 1964 when American Express collapsed in the market during the Tino De Angelis salad oil scandal. Studying the company carefully, he determined that the danger from those losses would be limited, while its basic strengths, the credit card operations and the travellers’ checks, would be unaffected. He bought heavily and saw the stock quintuple in the next five years. In 1969, the stock market was booming, even junk stocks were selling at premium prices, and Buffett couldn’t find bargains anywhere. He sent another letter to his partners:

“I am out of step with present conditions. When the game is no longer played your way, it is only human to say the new approach is all wrong, bound to lead to trouble and so on… On one point, however, I am clear. I will not abandon a previous approach whose logic I understand (although I find it difficult to apply) even though it may mean foregoing large, and apparently, easy, profits to embrace an approach which I don’t fully understand, have not practised successfully, and which possibly could lead to substantial permanent loss of capital”.

Buffett had an additional problem. He had become fond of some of his principal holdings, such as Berkshire Hathaway, and no longer wanted to sell them at all. That, obviously, put him in potential conflict with his investors, in whose interest it might have been to sell. So after 13 years, he decided to fold up the partnership. It had gained thirtyfold in its value per share, and through the addition of more than 90 members and the success of its investments had grown to over $100 million. Buffett’s profit participation as investor-manager, plus the compounding of his own capital, had made him worth some $25 million. Investors were given back their money and their proportional interest in Berkshire Hathaway (of which he became chairman). Three years after the partnership was liquidated the market went into the 1973-74 collapse.

Buffett (directly or indirectly through Berkshire Hathaway) was able to buy big pieces of some of his favourite “gross profits royalty” companies at giveaway prices: 8% of Ogilvy & Mather at 8, 16% of Interpublic, 11% of the Washington Post at 3, the Boston Globe, Capital Cities (an independent chain of television stations that also owns newspapers), Knight-Ridder Newspapers, Affiliated Publications, Media General and Pinkertons. Several have tripled or quadrupled since. He also bought into a number of banks and other companies that have so far been uninteresting in the market. Even when markets disagree with him, however, he is happy with his stocks as long as the underlying businesses continue to do well. At this juncture he is no longer trying to maximise his investment profits, but rather to indulge his collecting instinct and to enjoy himself “playing several different games,” in newspapers, insurance and other areas.

“If one is ever going to buy common stocks, the time to buy them is now,” said Buffett in mid-1979. “It screams at you”. The enormous advantage the independent investor has, Buffett says, is that he can stand at the plate and wait forever for the perfect pitch. If he wants it to come in exactly two inches above his navel and nowhere else, he can stand there indefinitely until an easy one is served up. Stock market investment is the only business of which that is true. You can not only wait for the bargain but for the particular one that you understand and know to be a bargain. Buffett observes that you might improve your investment performance by having a quota, a limit to the number of investment ideas you could try out in your life: one a year, for instance… or even fewer.

Swing, You Bum!

Many times, though, the investment manager lets his advantage be turned into a disadvantage. Feeling obliged to remain active, he swings at far too many pitches, instead of holding off until he has an absolute conviction. He seems to hear the clients howling, “Swing, you bum!”. When he was 11, for example, Buffett bought three shares of Cities Service preferred at 38. His sister, who was 14, thought that she had better follow suit and bought three shares too. The stock declined to 27, She asked him about it every day. Finally, it recovered to 40. To be rid of the headache and the questions, Buffett sold his stock and hers, making a total profit of $5, after commissions. The stock then went right on to 200! He never forgot the lesson. He points out that if, for instance, he had reported to his partners that 40% of their money was in American Express, or that he was heavily long silver futures, his partners would have been concerned, asked questions, mailed him things to read. At best, he would have wasted a lot of time; at worst, he would have been influenced by their reactions. He says it would have been like a surgeon carrying on a running conversation with the patient during a major operation.

Buffett recommends looking less at earnings per share than at return on capital, which is what produces the earnings. There are ways of manipulating earnings per share and earnings growth; growth on total capital is harder to play with. Buffett believes almost no one should ever go short, but if one does it is best to go short the entire market - a representative list - rather than stocks one considers overpriced. Ben Graham tried going short overpriced stocks. Three out of four times it worked, but the fourth time he would get murdered as an already overpriced stock was run up to the skies by public enthusiasm. Buffett says that the trading approach to the stock market is excessively difficult, like a tournament of bridge experts in which each player can see others’ cards. The stocks are being followed by some of the best brains in the world. When Buffett was buying Disney or American Express there was virtually no competition. Buffett agrees that it’s scandalous for Wall Street houses to encourage small investors to dabble in commodities. He says that one sometimes can analyse the long-term price outlook for a nonagricultural commodity, notably a metal. If the price gets way below production cost for an indispensable metal, it must eventually recover. But the prices of agricultural commodities are subject to weather and other vagaries of nature: investing in them becomes a matter of flair. Since he depends on analysis for success, Buffett never will invest in an agricultural commodity.

A generous target for total return on a stock portfolio would be 3% a year from the dividends, plus a 9% capital gain, or 12% in all. After a 50% income tax and a 30% capital gain, however, 1.5% is left from dividends and 6.3% from capital gain, a total of 7.8% after tax. And when the general market is selling for, say, 1.5 times its own book value, as a whole, the respectable return falls considerably from this level. From time to time you can get a similar return from good quality municipals, such as industrial revenue bonds, without the risks of stock ownership. At such a time, municipals are preferable to stocks. Buffett mentioned that he had negotiated a direct purchase from K Market of an industrial revenue bond earning 7.5%, which should do better than many stocks, after taxes.

For me, Buffett’s most important single message is his cry of alarm and recurring admonition to steer clear of the standard big American heavy industries requiring continuous massive investment. Most of these companies are in trouble. The cause is competition, over-regulation, rising labour costs and the like. The symptom is that just to stay in business many of these big industries need more money than they can retain out of reported earnings after paying reasonable dividends. To stay in the same place they require endless infusions of net new cash, like India or Egypt. To be sure, there are dividends on the new stock and interest on the new bonds that they constantly issue, but basically, these dividends and interest payments are only a loss leader to induce the investor to buy the new securities being issued. He has only an outside chance of ever seeing his principal again in real terms.

No Smokestacks

Buffett regards investing in the “smokestack” companies, the heavy industries whose obsolescence is often more rapid than their allowable depreciation, as, in essence, participating in a series of constant mandatory rights offerings, where you have to put up more money to maintain your percentage interest. Instead of distributing their earnings to the shareholders in dividends, these companies are to retain them to build more capacity, either to replace rapidly ageing facilities or to meet competition. This increases output, which further lowers profit margins so that the companies are even less able to make real money in their basic business. Discussing American Airlines, Buffett mentioned that it turns over its capital (including leased equipment and facilities) only once a year. On that basis, it would have to realise close to a 20% pretax profit margin on sales in order to net 10%. In fact, the company makes nothing like a 20% profit margin on its sales, which would, indeed, be one the highest profit margins in all industry.

Buffett once met a leading executive of a capital-intensive business giant at a time when the company was selling in the market for one-quarter of its replacement value. Buffett asked the executive; “Why don’t you buy back your own stock? If you like to buy new facilities at 100 cents on the dollar, why not buy the ones you know best and were responsible for creating at 25 cents on the dollar?”.

Executive: “We should”.

Buffett: “Well?”.

Executive: “That’s not what we’re here to do”.

And so concludes the article.

Thanks for reading,

Conor

Conor, great writing.

I live about 40 minutes from the GEICO headquarters in Virginia that the young Warren Buffett visited. Several times a year I get caught at the traffic light in front of the GEICO entrance, and I spend 2 minutes staring 👀 in full Buffett "fanboy" mode!

Thank you! I have always wanted to read that passage. Very kind of you.