In the words of the controversial financier, George Soros, “I haven’t given up the illusion that I have something important and original to say”. On October 30th, 2025, I was perusing my Twitter feed— a once enjoyable experience that has sadly decayed over the last few years. That is not the subject of today’s prose, however.

This day coincided with the third quarter earnings announcement from Chipotle Mexican Grill. The past few years have been tough for this once loved purveyor of proteins and vegetables. A few solid years of unabating global inflation had caused input costs to soar which, in turn, means menu inflation followed. It was around this period that Chipotle faced increasing backlash online about their portion sizes— both in terms of their inconsistency as well as the fact customers felt they were being shortchanged. Was this tactful internal policy to save margins or an unfortunately-timed gradual decline in the enforcement of standards? Who’s to say.

The fact of the matter is that this earned Chipotle a lot of bad press. So much so, that press releases and advertising campaigns were spun up to console angry customers and assure them more attention would be given to serving beefy portion sizes once more. A recurring theme throughout earnings calls of 2024 and 2025 was the company’s progress on setting the portion problem straight.

Below is a snippet from the first time the social media backlash was brought up during the company’s Q2 2024 results in July 2024.

“I want to take a minute to address the portion concerns that have been brought up in social media. First, there was never a directive to provide less to our customers. Generous portion is a core brand equity of Chipotle. It always has been, and it always will be. With that said, getting the feedback caused us to relook at our execution across our entire system with the intention to always serve our guests delicious, fresh, custom burritos and bowls with generous portions. To be more consistent across all 3,500 restaurants, we have focused in on those with outlier portion scores based on consumer surveys, and we are reemphasizing training and coaching around ensuring we are consistently making bowls and burritos correctly”.

- Brian Niccol, former CEO of Chipotle

Brian Niccol would leave shortly after, in August 2024, to join Starbucks. By November, Scott Boatwright, Chief Operating Office since 2017, was appointed.

The Coming of Slop

I don’t know exactly when the phrase entered the lexicon of the english-speaking world, but at some point Chipotle, and a handful of other quick-serve bowl-centric restaurants, began to adorn the title of “Slop”. Slop merchants. Bowls of slop. The era of slop. Slop fatigue. One of my favourite headlines1 read, ‘The slop bowl recession just sent Chipotle’s stock cratering’.

The date of this article was October 31st, 2025. The day after Chipotle reported their third quarter earnings for the year and the stock fell 18.2%. Only three times in history has the stock fell harder in a single day. Two occasions during the great financial crisis of 2008 when the company’s share price would fall ~20% within 2 months of each other. Once, in 2012, where Chipotle fell 22% after the E.coli scandal hit the headlines.

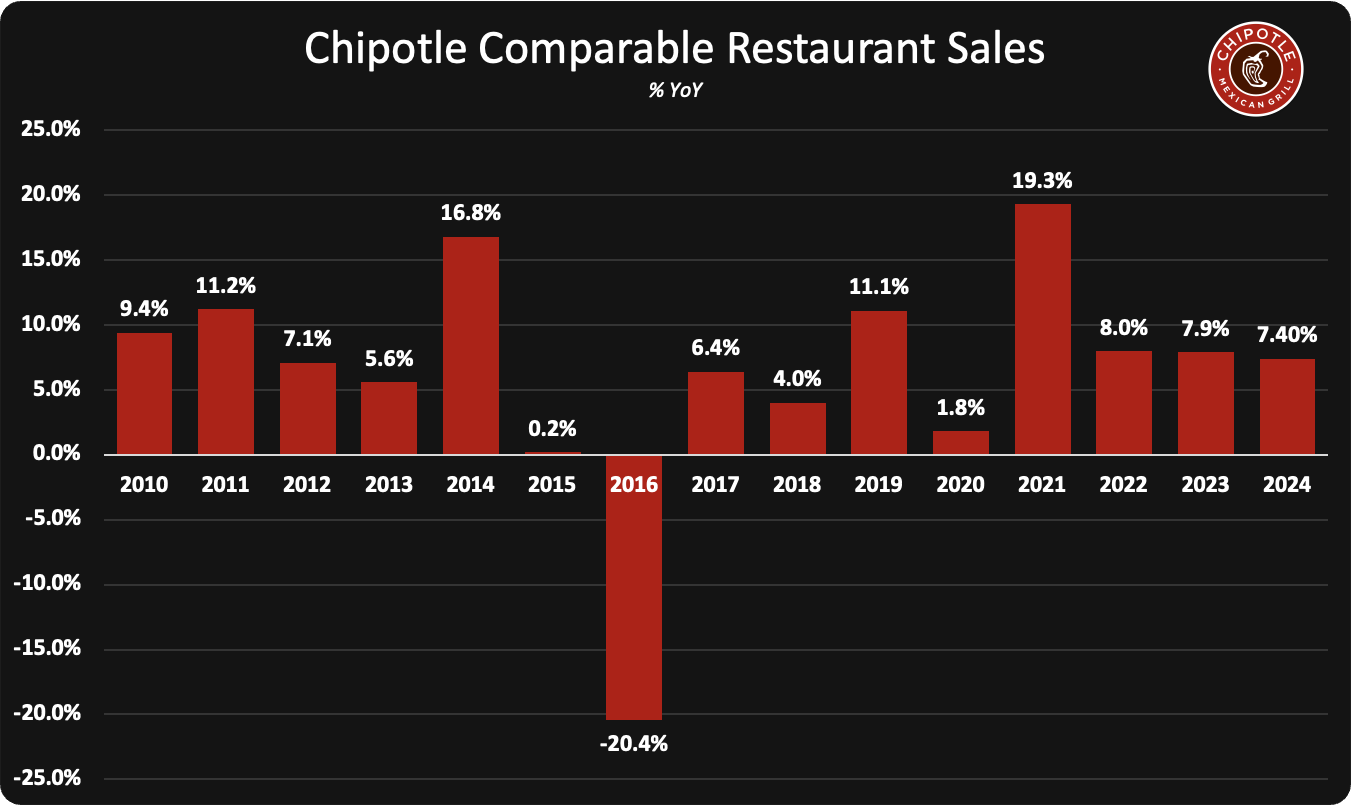

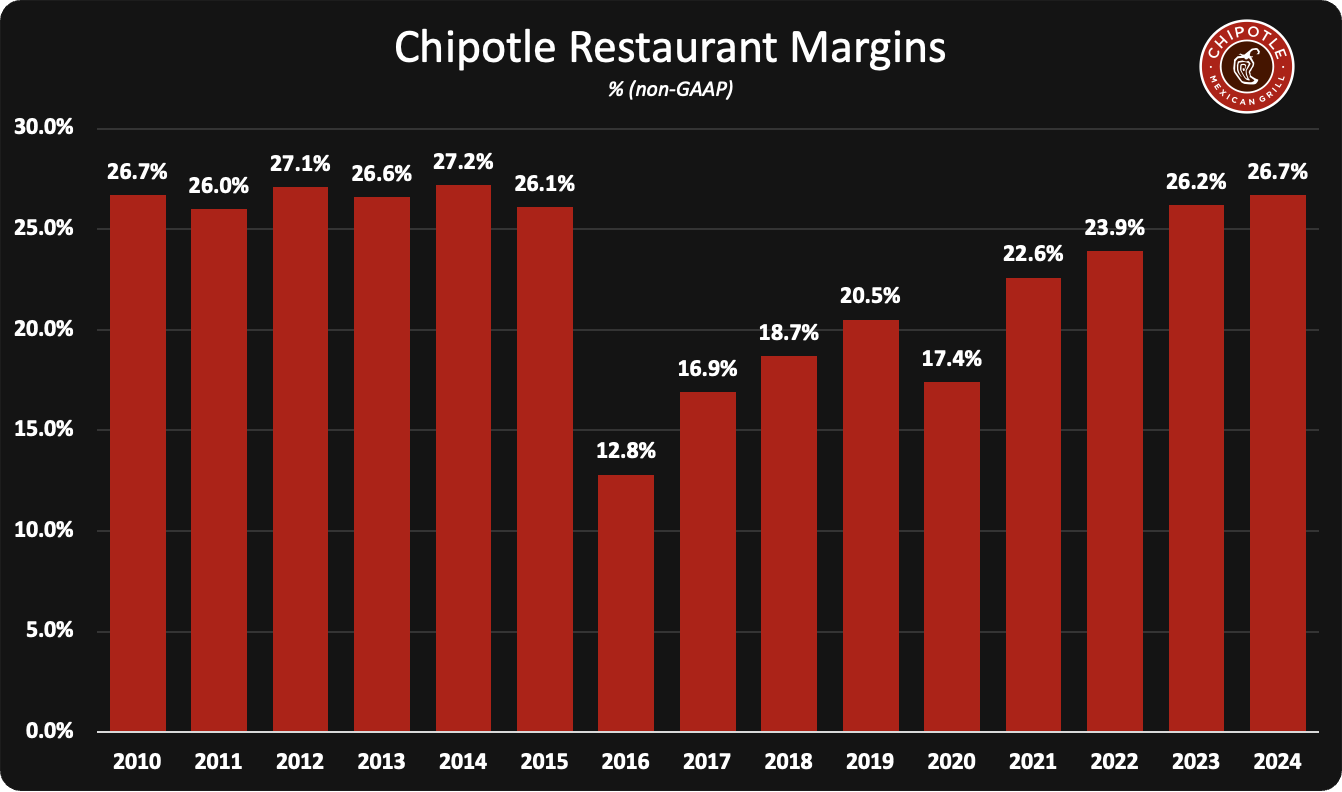

What was so calamitous in this earnings call that caused such a sudden recoil from investors? Following successive negative comparable sales, Chipotle managed to squeeze out a 0.3% improvement on comparable sales in that quarter. Restaurant margins decline 100bps YoY falling to a, still high by industry standards, 24.5%. Talks of macroeconomic pressures, results failing to live up to analyst expectations, yada yada yada. The objective truth of the matter is that Chipotle was still choking down the inflation from the post-pandemic era and it’s influence on the, now more sensitive, consumer.

With the mythical powers of hindsight, its clear that Chipotle sprayed the inflationary bazooka for a little too long. Instead of offsetting inflation, they were confident the consumer could absorb more price. Observing the 3 years before and after the pandemic (2020) are telling. In 2017, 2018, and 2019, Chipotle pushed through annual menu price increases of 1.2%, 2.4%, and 0.2%, respectively. In 2021, 2022, and 2023, the annual price hikes were 8.5%, 12.0% , and 5.2%. After pressure on transactions growth started to appear, Chipotle lowered the price inflation to 2.9% in 2024. Despite pushing price so hard, Chipotle’s consumers were unwavering. Comparable sales kept printing good numbers. Transactions, albeit with a wobble in 2022, continued to look strong too, with comps of 10.3%, 0.9%, 5.0%, and 5.3% in 2021, 2022, 2023, and 2024, respectively.

One could be forgiven for thinking that Chipotle knew something we didn’t. How could this business continue to raise prices even as inflation in the United States, Chipotle’s largest market, started to come back down to earth in early 2023? What made them so confident?

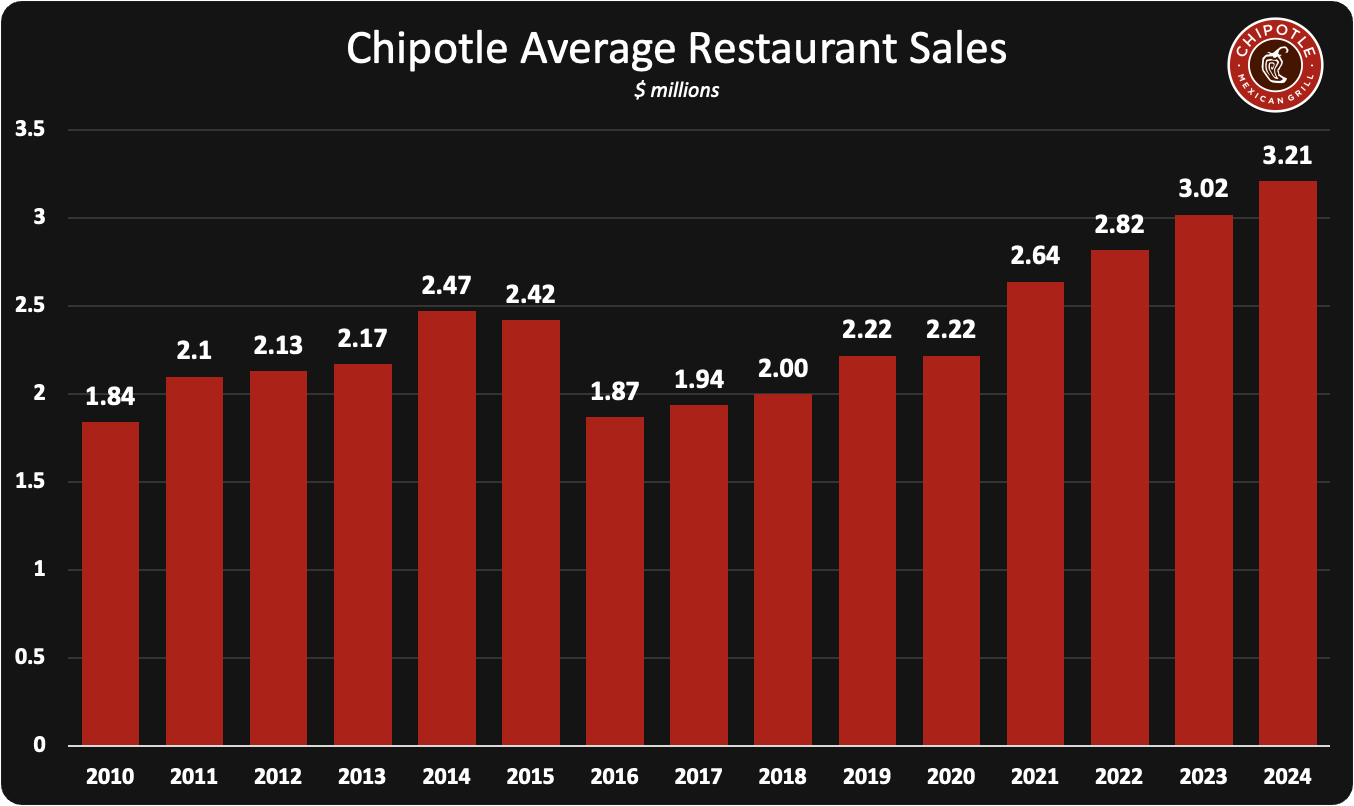

In early 2024, while discussing the company’s Q4 2023 results, former CFO John Hartung suggested that Chipotle could see restaurant-level margins as high as the “30% range” as the company approach $4 million average unit volumes.

“As we get up to $4 million, I would expect we’d be in the high 20%, maybe even in the 30% range. Again, you’re talking about predicting something over a very long period of time. But our margins will definitely get stronger over time, which means our returns will get stronger as well as we move from $3 million to $4 million”.

-John Hartung, former CFO of Chipotle

At the time, Chipotle had just reported 26.2%2 margins while simultaneously surpassing $3 million in AUV for the first time. In the following year, Hartung’s message would seem like gospel as margins increased 50bps and the AUV saw an incremental $190k improvement to $3.2 million.

All seemed well. There was some social media backlash against small portions. There was a change in CEO. The rise of the term “slop bowl” was becoming more prominent. But until around Q1 of 2025, Chipotle had showed few signs of fundamental deterioration. The stock marched on. By the end of 2024, Chipotle shares traded for ~$60 which was not too far away from the all-time high of $68.

Chipotle continued the inflation party long after the economy began signalling it needed a break and this ultimately came back to haunt them in 2025. In financial markets it only takes a few bad quarters for a story to “fall apart”. The first two quarters saw consecutive bouts of negative comparable sales. Counter narratives started forming. Margins begin to slide and so too did the share price.

If there is one thing you can count on, its the high correlation relationship between falling share prices and headlines declaring the end times for said company. In a lot of cases, this is apt. In some cases, and this is where you are paid as an investor, its a simple case of narrative following price. In the case of Chipotle, it is my opinion that the challenges facing the company are temporal. Nature catching up with a company that overreached in price without an accompanying increase in quality. Nature eventually striking down those who traded on borrowed time. We’ve since seen Chipotle make a strong effort to bring value back to the menu with incredibly low priced, protein packed, offerings. Smaller tacos, protein bowls with 32g protein under $4. It’s not exactly my cup of tea, but it’s an obvious boon to the add-on business as well as something to satiate the cheapskates.

In my mind, it doesn’t take a lot to put Chipotle back on track. In my opinion it never really derailed, but in the eyes of the fickle analysts, it has. Chipotle has an incredibly efficient box-box scaling model, high margins that can take a punch or two, and a largely untapped global market outside of the United States, where more than 95% of their stores are located.

Following the intra-day dump of Chipotle on October 30th, I picked up shares for the price of $30 a piece. I find it laughable that commenters claim that Chipotle is finished. Like there is not a world outside of the borders of the U.S of A. I don’t expect much in the 2025 fiscal year results. Revenue will grow at a subdued rate. Margins will likely contract. Comparable sales are going to decline for the first time since 2016. Much of this was priced in the second it became apparent to the market, many months back.

As for 2026, I see it probable that an improvement on 2025 results will occur. From there, I think the narrative will eventually shift back to business as normal. Maybe next year, maybe the one after that. Maybe the crowds shouting “Slop” will get bored and move onto the next struggling industry, who knows. I don’t invest on two-year time horizons. I am not skilled, nor lucky enough to do so. I have heard that longer time horizons improves the odds of getting lucky. Lord help me. At $30 per share, I think much of the downside is accounted for.

Thanks for reading,

Conor

Good call so far 😀

Protein bowls with 32g protein under $4 is quite a treat!

Thank you, cheers!